The livestock and poultry industries account for nearly half of South Africa’s farming fortunes. So when there are frequent cases of animal disease, there tends to be panic about the impact on growth. In recent years the cattle industry has struggled with foot-and-mouth disease, leading to temporary closures of some key export markets and an increasing financial burden on farmers.

The department of agriculture, in collaboration with organised agriculture, has explored ways to contain the spread of the disease. Still, its ongoing occurrence and severity this year compelled South Africa to adjust its longstanding approach to addressing foot-and-mouth disease and transition to national vaccination. We welcome this decision and believe that if executed well it will help the country control the disease.

South Africa is not the first country to take this path. Argentina and Brazil are among the countries that have opted for vaccination against foot-and-mouth disease in cattle. When any country has managed to control the disease, vaccination typically stops or pauses.

The scale of this work will be challenging, as South Africa has a cattle herd of over 12-million, according to the “Abstract of South African Agricultural Statistics” from the department of agriculture. Co-operation with commercial farmers, agribusinesses, organised agriculture and communities will be vital to ensure the success of the vaccination process.

Significantly, South Africa currently relies on imports of the foot-and-mouth disease vaccine, mainly from Botswana. In this new approach, diversifying import sources to include countries such as Turkey should be a key consideration. The work to revive the Agricultural Research Council (ARC) and Onderstepoort Biological Products (OBP) to produce the essential vaccines domestically is key and must gain momentum.

South Africa must also ensure that other private sector stakeholders are part of vaccine production. Private labs must be included in the vaccination production to diversify the supply and ensure domestic availability in the future.

From a consumer perspective, South Africa’s beef and livestock products are safe to consume.

Moreover, in our view, the start of national cattle vaccination is unlikely to introduce major upside risks to meat price inflation. The vaccination process does not change the path to easing food price inflation in South Africa.

We believe that the vaccination process is likely to be phased, allowing continuous slaughtering at the normal pace. In the medium term, efforts to control the disease also bring some normality to the slaughter process and ease price volatility.

We are highlighting meat because it has been one product in the food basket that has exerted upward price pressure after the announcement of a foot-and-mouth disease outbreak in major feedlots led some retailers to panic.

This, however, has now eased, and meat price inflation is slowing, contributing to the general easing of food price inflation in November 2025.South Africa’s consumer food price inflation slowed for the third consecutive month, easing to 3.9% in October, from 4.4% in the previous months.

The primary drivers of the deceleration were mainly fruit and nuts, vegetables, meat, sugar, confectionery and desserts. Ample supplies, combined with the base effects, contribute to the easing of price inflation in these products.

While modestly up from the previous reading, cereal products inflation also remains relatively low on the back of the ample grain harvest. South Africa’s 2024/25 summer grains and oilseed harvest is estimated at 20.08-million tonnes (up 30% year on year). The various fruits and vegetables also delivered ample harvests.

Overall, we remain optimistic that South Africa’s consumer food price inflation will continue to moderate. The benefits of lower grain prices, ample fruit and vegetable supplies and potentially easing meat prices will continue to be the major drivers of the deceleration. We don’t see meat as a significant upside risk on prices.

The challenge of foot-and-mouth disease in South Africa is not over and continues to put pressure on farmers, even as vaccination is under way. Typically, during foot-and-mouth disease outbreaks, the country is temporarily closed to some export markets, leading to a drop in consumer prices.

But this year we saw the opposite. Initially, panic buying driven by retailers’ announcements, rather than a product shortage, was the main driver of meat prices, combined with buoyant consumer demand. We now see an easing of these upward price pressures. As the vaccination process gains momentum in the coming months, we expect to see more normalisation.

If you enjoyed this post, please consider subscribing to my newsletter here for free. You can also follow me on X (@WandileSihlobo)

The practices of some countries in the Southern African Customs Union (SACU) are worrying. We continuously see countries restricting imports of agricultural products on short notice, with limited communication to other countries.

Namibia and Botswana are the major culprits of this practice. They blocked South Africa’s vegetable imports in 2021 and at various points in subsequent years.

But in Botswana, when the new President, Duma Boko, came into office, he lifted the bans imposed by the previous administration, as inflationary pressures continued to bite households.

Disappointingly, I learned this morning that the Botswana government is again imposing bans on vegetable imports and forcing consumers to buy local. The Botswana government notice of December 8, 2025, includes a restriction on imports of tomato, potatoes, white cabbage, red cabbage, white onion, red onion, watermelon, green papaya, beetroot, carrot, lettuce, strawberry, ginger, red and yellow peppers, garlic, and butternut.

I sympathise with supporting local farmers and reducing their dependence on South Africa. But I am uneasy with the drastic policy changes, with minimal consideration for regional ambitions.

Among other things, my source of frustration with these restrictions is that these countries are all part of the Southern Africa Customs Union (SACU). This bloc promotes free trade and economic integration.

Nevertheless, the SACU agreement contains a loophole that allows such restrictions. The SACU Agreement states that ‘Article 18 (2) … notes that Member States have the right to impose restrictions on imports or exports for the protection of: health of humans, animals or plants, the environment, treasures of artistic, historic or archaeological value, public morals, intellectual property rights, national security and exhaustible natural resources.’

But I don’t see the current Botswana restrictions fitting the above description.

Of course, this action has had a financial impact on South African farmers, who have for many years produced for the domestic market and the region at large. The question that remains is: how should we respond to these events?

South Africa’s response will need to be sensitive but firm. While all this is frustrating, we should not be antagonistic or arrogant, but rather see this through the lens of understanding Botswana’s aspirations, formulate pathways for coexistence, and ensure better communication of policy approaches within the region.

Having hostile neighbours will not benefit any of these countries’ citizens. After all, people primarily want affordable, accessible and safe food. Botswana could therefore close the market in specific windows to boost domestic production and should clearly communicate this to South Africa. The South African producers would then fill specific windows when gaps occur in these markets.

For long-term planning, it would also help if these countries communicated to South Africa which agricultural products they deem ‘national security or sensitive’ and which they want to boost their domestic production of over the years.

This would help better plan the agricultural export drive to other regions and progressively reduce dependence on its neighbours. Importantly, these import bans should not be perpetual but have time limits once Botswana’s producers have restarted their industries and can compete in open markets with South Africa.

The growth or desire to expand agricultural production in these countries also has a positive spillover effect on South African agribusiness, which can supply farm implements and inputs to them. Botswana should remain open and not hostile in this respect.

These Southern African countries should revive the regional spirit and formulate agricultural policies and programmes from that perspective.

I must also state that South Africa has benefited significantly from exports to the African continent. For example, in the record agricultural exports of US$13.7 billion in 2024, the African continent accounted for roughly 40% of the destinations. This figure has been the same for the past decade.

Importantly, for every dollar of agricultural products South Africa exports to the African continent, 90 cents are traded within the Southern African region. Thus, an engagement with this region on the export ban must recognise that South Africa, as a country, depends heavily on the Southern Africa region.

In essence, we must ensure that SACU works for all and that South African industries don’t become disadvantaged by poor policy communication in the region. Overall, as these issues continue, there is value in reviewing SACU and its benefits for all members. This review is now also about broader trade policy, as South Africa seeks to expand its export markets and is often hindered by SACUS-related issues. But I will have a lot to say about that someday.

If you enjoyed this post, please consider subscribing to my newsletter here for free. You can also follow me on X (@WandileSihlobo)

Domestic policies generally guide agricultural developments here at home. That said, gatherings such as this past weekend’s G20 Summit always provide an opportunity to mobilize support and generate global policy discourse around particular issues.

These gatherings also provide an opportunity for policymakers and business leaders to connect with other countries and strengthen ties. This was particularly the approach of South Africa at the G20 Summit.

For example, the South Africa–European Union (SA-EU) Bilateral Summit on November 20, emphasized the need for cooperation, investment and deepening trade. Various agreements and Memoranda of Understanding (MoU) were signed, including those on critical minerals and energy.

For us in agriculture, deepening relations with the EU, one of our most important export markets, is key to the long-term growth of the sector in this fractured global trade order.

While South Africa has faced challenges across various sectors, including citrus, poultry, and beverages, the EU remains one of its critical trading partners.

In 2024, the EU was South Africa’s third-largest agricultural market, accounting for 19% of our US$13.7 billion in exports. Citrus, grapes, wines, dates, avocados, pineapples, fruit juices, apples and pears, berries, apricots and cherries, nuts, and wool are amongst the top agricultural products South Africa exported to the EU.

Notably, the EU has remained South Africa’s major trading partner through to 2025. In fact, in the third quarter of 2025, the EU remained South Africa’s third-largest agricultural market, accounting for a 23% share of US$4.7 billion in exports.

On November 21, South Africa also had another critical bilateral meeting with Australia. We do not typically consider Australia when we think of trade in South African agriculture.

However, we have trade in other sectors, such as the automotive industry, and investments across various other sectors of the economy.

South Africa and Australia’s agricultural sectors are more similar. Still, there remains room for collaboration between our countries in a range of areas that could further boost our agricultural sectors.

One area we can draw on from the Australian experience, which is urgent for us in South Africa, is biosecurity. We are currently struggling with foot-and-mouth disease in South Africa’s livestock industry, and a collaboration with Australia in this area would be valuable.

Moreover, Australia’s work on climate-smart agricultural practices and its cooperation with the private sector to advance research are other areas of learning for South Africa.

The Australian government equips farmers with sound research and pathways to reduce emissions and produce in more environmentally friendly ways. These are also vital to global agricultural trade today.

Therefore, these high-level bilateral meetings between South African and Australian political leaders are essential in opening a pathway for more direct engagements at the departmental and industry levels.

Also on November 21, we saw South Africa sign an MoU on agricultural matters with Vietnam. The MoU focuses on expanded cooperation in crop production, plant protection, animal husbandry, veterinary services, research, development, technology transfer and agricultural trade. These are all key areas for our farming sector.

Admittedly, the MoUs won’t lead to sudden changes or the opening of markets. Trade agreements are needed for that. Still, they help maintain close relationships and collaboration, which are key to establishing trade agreements.

Vietnam is a market we keep on our radar in agriculture. The country spends over US$30 billion on agricultural imports annually. But if one looks at Vietnam’s agricultural products suppliers, South Africa doesn’t feature prominently. South Africa ranked 34th among agricultural suppliers to Vietnam.

In 2024, Vietnam imported US$34 billion worth of agricultural products. South Africa accounted for only 0.3% of these imports (about US$89 million). The key suppliers of agricultural products to Vietnam were China, Brazil, the United States, Argentina, Cambodia, Australia, India, and Indonesia, collectively accounting for 70% of the country’s agricultural imports.

This happens, although the products Vietnam imports are generally similar to those South Africa exports to various parts of the world. Among other things, the hindrance to trade remains tariffs and phytosanitary barriers. These could be resolved through trade agreements. Still, the path to such agreements will benefit from cooperation, as seen in these MoUs.

In essence, South Africa’s agriculture is export-oriented, and already exports roughly half of the agricultural produce in value terms.

The G20 networking opportunities helped the country take a step forward in reaffirming its commitments to existing trade relations, such as with the EU, while starting conversations with new partners, including Vietnam.

These are not the only engagements that benefited agriculture, but we highlighted them as an example.

However, we stress that more work lies ahead to turn these engagements into long-lasting economic opportunities. That work must start immediately.

If you enjoyed this post, please consider subscribing to my newsletter here for free. You can also follow me on X (@WandileSihlobo)

As the northern regions of South Africa receive excellent summer rains that help summer crops, the south-western areas of the country have been relatively warm and dry. The warm weather helps with the winter wheat harvest. The farmers are making encouraging progress.

I am looking at the wheat delivered to commercial silos between September and the end of November, which is about 1.1 million tonnes. This volume equals 55% of South Africa’s expected 2025-26 wheat harvest of 2.03 million tonnes. By the way, the harvest is up 5% from the 2024-25 season.

The annual improvement is boosted by the expected better harvest in the Northern Cape, Free State, Eastern Cape, and Limpopo.

The Western Cape, which accounts for over half of South Africa’s winter wheat production, is expected to experience a mild decline in the harvest this year compared to the 2024-25 season due to unfavourable weather conditions in some parts of the province.

A potential wheat harvest of 2.03 million tonnes implies that South Africa may need to import approximately 1.74 million tonnes in the 2025-26 season to meet our annual needs.

These imports are expected to be down 5% from the 2024-25 season. The import activity is unlikely to pose a challenge. We have ample global wheat supplies, which will ease South Africa’s import activity. For example, the International Grains Council forecasts a record 2025-26 global wheat harvest of 827 million tonnes, up 3% from the previous season.

With the domestic wheat production figures we have at hand, combined with global wheat supplies, we view the situation as boding well for a moderating path of food price inflation.

Evidently, we continue to see lower wheat prices. South Africa’s wheat spot price was R5,636 per tonne on December 2, 2025, down 5% year-on-year.

If you enjoyed this post, please consider subscribing to my newsletter here for free. You can also follow me on X (@WandileSihlobo)

One aspect I have highlighted frequently in this letter is the prospect of an uneven recovery in South Africa’s farming fortunes in 2025.

On the positive side, ample grain, oilseed, sugarcane, fruit, wine, and vegetable production support annual recovery.

Meanwhile, on the negative side, foot-and-mouth disease continues to add pressure to the sector. The livestock and poultry account for nearly half of the farming sector’s fortunes, and therefore, when they experience challenges, the entire sector feels the impact.

While the subdued performance remains encouraging, it does also dwarf the excellent performance in the various crops.

For example, South Africa’s 2024-25 summer grains and oilseeds production is at 20.2 million tonnes, up by 30% from the previous year. This figure comprises maize, soybean, sunflower seed, groundnuts, sorghum, and dry beans.

In the case of maize, we have the second-largest harvest on record, and in soybeans, the largest on record due to favourable La Niña-induced rains. The various fruits and vegetables also achieved excellent harvests, as reflected in healthy export volumes.

Still, the primary challenge for cattle is the foot-and-mouth disease. South Africa will start vaccinating its roughly 12 million cattle. The vaccination will take a while, and the logistics of carrying it out and sourcing the vaccine remain the primary focus. That said, a plan is in place to address the challenge.

Overall, this third-quarter growth underscores the view that agriculture will generally recover in 2025, albeit likely a mixed recovery from a subsector perspective. Notably, the sector is poised for better performance in 2026, as La Niña rains are expected to persist, supporting production.

If you enjoyed this post, please consider subscribing to my newsletter here for free. You can also follow me on X (@WandileSihlobo)

I have no issue with what the Eastern Cape Premier, Mr Oscar Mabuyane, writes this morning in the Daily Dispatch, a local newspaper. Among other things, he outlines the benefits of the recent upgrades to the N2 Highway Wild Coast, which are expected to ease logistics in the region.

Mabuyane also outlines the promise of the digital infrastructure rollout underway, the upgrades to Mthatha airport, and the gains they will bring, particularly in rural regions.

Other aspects he writes about include potential water infrastructure projects, the promise of tourism, and agriculture, among other sectors.

In essence, I support some of these interventions. What we need is focused implementation.

You see, I have been troubled for some time by the Eastern Cape’s sluggish economic progress, higher unemployment, poverty, and the provincial government’s inept service delivery.

Admirable progress

And yes, I know there has been some good work in various regions of the province. For example, the national road network from Port St Johns to Gqeberha is in admirable condition following recent improvements, and Premier Mabuyane correctly highlights it.

This has improved travel ease and supports businesses, especially agribusinesses that rely heavily on these road networks.

New schools and clinics have recently been built in rural regions. These have led to some green shoots in terms of education outcomes.

Troubling areas

In areas that need enormous improvement, we must focus on municipalities that remain in a troubling space.

Another area of neglect is road maintenance and service delivery in various towns, especially the former Transkei region.

Poor rural roads, water challenges, higher crime rates, and poorly maintained towns, among other issues, are slowing the province’s fortunes.

All these weigh negatively on farmers and small businesses that struggle to connect with clients in business centres, leading to financial losses due to higher transaction costs.

In addition to the automotive industry, agriculture and agro-processing, various services, tourism, and agrotourism are some industries the Eastern Cape should be driving.

However, the province has not made admirable progress in these areas. Even if the province promoted tourism, with these long-running problems, businesses would struggle to attract more clients to the province for the long term.

Yes, we have a great province that can offer so much and, in the process, create jobs.

The Premier of the Province, as he has done today in the Daily Dispatch, typically gives promising speeches that diagnose the underlying problems.

But the delivery remains disappointing. For example, in agriculture, the province still has a sharp dualism. The former Ciskei regions of the province, with dominant commercial agriculture, are the engine of the provincial agricultural fortunes. Meanwhile, the former Transkei region remains at the periphery of progress.

The region faces challenges in land governance, inadequate infrastructure (roads, water, silos, etc.), and the absence of organised agricultural training.

As a result, there are tracts of underutilised land in regions with favourable rainfall. The province’s leadership should pull all the stops to ensure we realise agricultural growth in the province.

Progress in provincial agriculture would be an engine for addressing high unemployment and poverty. These would also be highly technical jobs in the value chain.

The other industries that could thrive are tourism and agritourism.

The Eastern Cape has the potential. However, its leadership must do its part seriously to restart the province.

Once we see their efforts, the private business will follow up and invest. We can’t keep having a rural province with a “potential” never achieved while people suffer.

While I have placed the burden on the Premier’s hands, the people of the Eastern Cape must define their destiny.

Pockets of fertile lands remain fallow. People seem to have lost hope in farming for various reasons, which I have discussed above.

The government has also done little to build confidence and provide the necessary infrastructure and a conducive operating environment to return intellectual and physical capital to the province.

Provided agriculture could be revitalised, supportive infrastructure, agriculture, and agribusiness could create far more economic opportunities than we see in some urban regions.

In essence, the problems of the Eastern Cape lie in the need for better governance and focused implementation of what the provincial leadership has long discussed, and the Premier outlines again in this latest Daily Dispatch essay.

If you enjoyed this post, please consider subscribing to my newsletter here for free. You can also follow me on X (@WandileSihlobo)

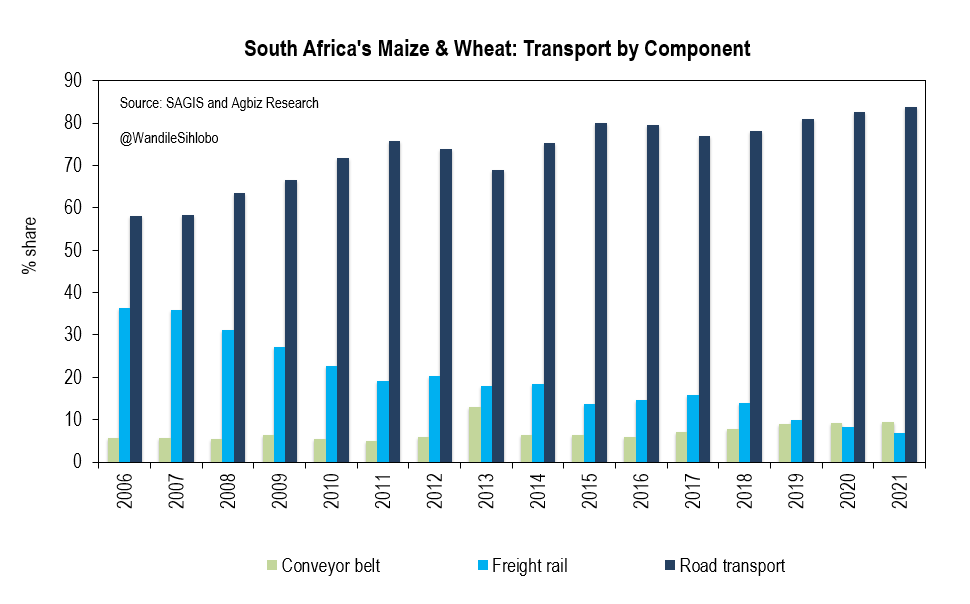

The expected increase in fuel prices on 03 December 2025 comes at a busy time for South Africa’s agriculture, as we continue summer grain and oilseed plantings. The diesel price (0.05% wholesale inland) could increase by 61 cents per litre, while the petrol price (95 ULP inland) could increase by 26 cents per litre.

Fuel accounts for a notable share of grain farmers’ input costs, about 13%. We are also in a busy period for winter grains and oilseeds, with harvest underway.

Beyond farmers, agribusinesses are also exposed to fuel price increases, particularly in logistics. It is worth noting that roughly 81% of maize, 76% of wheat and 69% of soybeans in South Africa are transported by road.

On average, 75% of national grains and oilseeds are transported by road, as is a substantial share of other agricultural products.

If you enjoyed this post, please consider subscribing to my newsletter here for free. You can also follow me on X (@WandileSihlobo)

He is a Senior Lecturer Extraordinary at the Department of Agricultural Economics at Stellenbosch University.

Sihlobo is also a Visiting Research Fellow at the Wits School of Governance, University of the Witwatersrand, and a Research Associate at the Institute of Social and Economic Research (ISER) at Rhodes University.

Sihlobo was appointed as a member of President Cyril Ramaphosa’s Presidential Economic Advisory Council in 2019 (and re-appointed in 2022), having served on the Presidential Expert Advisory Panel on Land Reform and Agriculture from 2018.

He is also a member of the Council of Statistics of South Africa (Stats SA) and a Commissioner at the International Trade Administration Commission of South Africa (ITAC).

Sihlobo is a columnist for Business Day, The Herald and Farmers Weekly magazine.

He holds a Bachelor of Science degree in Agricultural Economics from the University of Fort Hare and a Master of Science degree in Agricultural Economics from Stellenbosch University.