As we begin the 2025-26 summer season, the evolving weather conditions will remain a central focus in South Africa’s agriculture. We are in another year of La Niña, a weather phenomenon that typically brings above-normal rainfall in much of the country and the Southern Africa region.

The 2024-25 season was another La Niña season, and with its heavy rains, we experienced challenges in various areas of the country. Still, the overall picture was positive. We managed to get an excellent fruit and vegetable harvest. The sugar cane production recovered, and the grains and oilseeds production was also robust. It is due to such an exceptional harvest that you have seen me write about 2025 as a season of recovery in South Africa’s agriculture, albeit an uneven one, because of the foot and mouth disease in cattle farming.

Indeed, there will likely be heavy rains, but I don’t believe they are severe enough to warrant concern about the agricultural outlook for the 2025-26 season. We remain broadly optimistic about the season ahead.

In fact, the farmers are also as optimistic and have started preparing the land in the eastern regions of the country. Over the past two weeks, we observed activity in some areas of Gauteng, the Free State, KwaZulu-Natal, and the Eastern Cape. These are mainly yellow maize and soybean growing regions, crops that are key to the livestock industry. We will likely see an increase in field work with farmers tilling the land from November onwards.

The La Niña-induced rains may persist through to February 2026, a key period for summer grains and oilseeds. If the 2025-26 summer grain and oilseed production season continues with minimal interruptions, as we expect, the crop could pollinate around February 2026.

The crop requires increased moisture during the flowering or pollination stages. This coincides with the rainy period within the above forecasts, which supports the crop, and underscores our optimism about the upcoming season.

In essence, our optimistic expectations for the 2025-26 summer season seem to have some early support, as fieldwork activity has started on time in the eastern regions of South Africa. Whether farmers plant the typical area for summer grains and oilseeds or not is something we will watch closely in the coming months.

Our general view is that plantings will be robust and aligned with the previous season, at about 4.5 million hectares.

Therefore, while there may be periods of excessive rains in some regions, I think it remains fair to view the 2025-26 agricultural season with some optimism.

If you enjoyed this post, please consider subscribing to my newsletter here for free. You can also follow me on X (@WandileSihlobo)

This is an update from the post I made last weekend. I may regularly comment on this as we receive South Africa’s grain trade data weekly. October 10 marked the second week of the new 2025-26 marketing year.

The imports to date have totalled 92,705 tonnes from the United States, Australia, Lithuania, and Poland. The United States was the new addition this marketing year, while the rest of the countries were the primary suppliers in the first week of the 2025-26 marketing year. The year ends in September 2026.

We expect South Africa’s 2025-26 wheat imports to reach 1.74 million tonnes, down from 1.83 million tonnes in 2024-25 marketing year because of an expected slight recovery in the domestic harvest.

Some background

For anyone wondering why South Africa imports wheat, I must highlight some brief historical perspective I have shared here before. South Africa began importing over a million tonnes of wheat from the 2003-04 marketing year.

In the years before that, wheat imports averaged 458,518 tonnes, for example, between 1989-90 and 2002-03. The import surge resulted from increased consumption and a decline in area plantings.

From the 1997-98 season, South Africa’s wheat plantings fell below a million hectares, the norm in seasons before this period. This decline is better explained by the profitability challenges that farmers have faced since that period, specifically in the Free State and in non-conducive climatic conditions.

The critical thing to recall is that before 1997-98, South Africa’s agricultural markets were regulated, and the various commodities boards played a massive role in setting prices, including wheat.

Thus, after deregulation, South African farmers had to compete in the global market. Therefore, the Free State production areas came under profitability strain, resulting in farmers switching from wheat to other profitable crops.

Other provinces of South Africa don’t have large areas with conducive climatic conditions for high-quality wheat milling for human consumption. Hence, we speak of a few central wheat-producing provinces, including the Western Cape and those under irrigation in the Northern Cape, Free State, Limpopo, and North West.

A significant development over the years has been the improvement in productivity in South Africa’s wheat farming. In 1997-98, South Africa’s wheat yields were below 2.0 tonnes per hectare. The yields are 3,8 tonnes per hectare as of the 2024-25 production season.

Because of improved profitability, South African wheat production has remained relatively large. The 2021/22 crop was the largest in 20 years, at about 2.3 million tonnes.

In 2025-26, the crop is estimated at 2.03 million tonnes. This is insufficient to meet annual consumption. Thus, we say, South Africa will likely import about 1.74 million tonnes of wheat in the 2025-26 marketing year to supplement the domestic supplies. The current import volumes are roughly half of South Africa’s annual wheat needs of 3.8 million tonnes.

If you enjoyed this post, please consider subscribing to my newsletter here for free. You can also follow me on X (@WandileSihlobo)

Since South Africa’s Department of Agriculture held its seminar on the Agriculture and Agro-processing Master Plan, which seeks to unlock inclusive growth in the sector, I have noted some pushback from various corners.

But some of this came as a surprise, as the Agriculture and Agro-processing Master Plan broadly crystallises much of what Chapter Six of the National Development Plan already outlined. Its value is a sharper focus and granularity it presents in its interventions, with a highlight on commodity corridors, and deeper value chain analysis.

These enable us to plan to have a more focused suggestion about what to correct to unlock growth in each value chain. There are also proper structures for continuous interaction and evaluation of actions of the stakeholders throughout the implementation process.

Therefore, I see those pushing for further debates as contributing to the issue many South Africans have complained about: the lack of implementation of policies and programmes. The reality is that there are many things we can debate in South Africa’s agricultural sector, such as the climate change policy, trade policy, and land reform, amongst others.

But the Agriculture and Agro-processing Master Plan has been discussed at length and perhaps does not require further debate, only implementation.

The Agriculture and Agro-processing Master Plan is the correct plan for unlocking growth and boosting inclusivity. It matters not who drafted this plan and who signed it. This is a sound plan, with the potential to improve our agricultural sector and address many growth-inhibiting factors fundamentally.

Such factors include, amongst other issues, the release of government land with title deeds to appropriate selected beneficiaries, improving biosecurity controls (plant and animal health), addressing crime, maintaining roads, rail, and ports, and improving local municipalities.

Some may not agree with all of the contents of the Agriculture and Agro-processing Master Plan, but we could start by implementing areas where there is common interest and consensus. Importantly, this is not a government plan; it was co-created by all stakeholders.

Therefore, implementing and making difficult decisions about dealing with officials who may constrain progress and private sector collaboration should be a primary focus of the leadership at the Department of Agriculture.

Worrying about who signed the plan and who wrote it is not an enriching path; what matters is whether the plan speaks to the core issues and is being implemented.

Another issue I want to comment on is trade, as it continues to dominate our conversation. I can’t emphasise enough that the growth path for South Africa’s agriculture involves a strong push for export diversification and the retention of existing export markets. So, in all the global travel and interactions with foreign representatives, this should be one of the key points we continue to table.

This also means we must continue to enhance our capacity as a country to engage productively with many countries on trade matters to ensure our success.

The effort requires both business and government to adopt a collaborative approach. I am sure that other sectors of the economy, such as the auto industry and mining, are of a similar view.

In agriculture, we still have the capacity to create more jobs and expand production. The success of this will depend on the efficiency of our efforts to open markets, while concurrently addressing the domestic matters that constrain production.

There are clear plans on how each of these issues should be tackled, and what is missing is the consistent and relentless focus on implementation.

If you enjoyed this post, please consider subscribing to my newsletter here for free. You can also follow me on X (@WandileSihlobo)

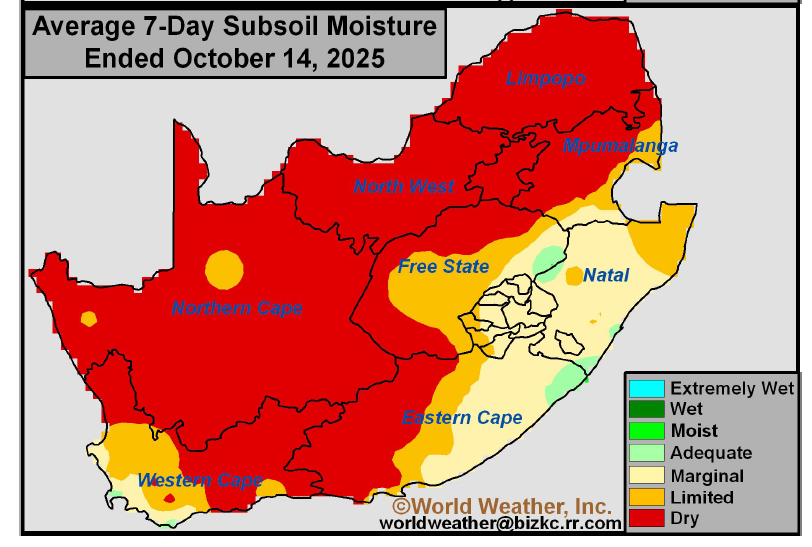

With South Africa’s 2025-26 starting already, we will continue to pay close attention to the weather outlook and soil moisture. This is key for planting and crop development, and the general agricultural season.

We are coming from a winter season, and the soil moisture, to some extent, mirrors this; it is relatively low. We will likely see some improvement after the first summer rains. Still, the plantings are underway in the eastern regions of the country.

I recently took a road trip from Gauteng to the Eastern Cape, through KwaZulu-Natal, which allowed for some field work assessment. I was happy with what I observed, as the planting has generally started in several areas.

We are in another season of La Niña rains, which means that we are likely to receive above-normal rainfall in the coming months. This is supportive of agricultural activity.

Therefore, when one sees a map of low soil moisture for now, as the one in this letter, there is no need to worry; this is a result of the winter season. We are heading to a rainy summer, and the farmers are busy in the fields, tilling the land for the 2025-26 season, which promises to be favourable. The farmers in the eastern regions will immediately benefit from better soil moisture conditions. The rest of the country will get favourable showers soon.

If you enjoyed this post, please consider subscribing to my newsletter here for free. You can also follow me on X (@WandileSihlobo)

The President delivered a vital speech today in Cape Town about food insecurity issues in South Africa. He correctly highlighted the household poverty challenges and emphasised the need to find numerous ways of addressing the food insecurity crisis in the country.

Income poverty (which requires an increase in job creation) is one aspect. Inefficient logistics and higher energy prices are among the pressures in the food value chain; thus, we remain with relatively higher food prices, even in times of ample harvests.

Still, the fact that we have a solid agricultural sector, with surpluses, helps a great deal in boosting food security at a NATIONAL LEVEL.

Moreover, another reason for household food insecurity is the low and stagnant growth, which contributes to unacceptable levels of unemployment. On top of this, South Africans spend a significant portion of their wages on transport costs due to the collapse of our public transport system. Ultimately, the country should deal with the constraints to growth, investment and employment.

If you enjoyed this post, please consider subscribing to my newsletter here for free. You can also follow me on X (@WandileSihlobo)

It is a reasonably busy day. But I do want to comment on the exciting news of South Africa’s signing of the stone fruit trade protocol with China. As South Africa’s Department of Agriculture stated:

“The agreement opens the Chinese market for the first time to five types of South African stone fruit, namely apricots, peaches, nectarines, plums, and prunes. It is also the first instance where China has negotiated access for multiple stone fruit types from a single country under one deal.”

This is commendable, and we must continue working to broaden South Africa’s agricultural access to China.

At the moment, South Africa holds a small share in China’s list of agricultural suppliers, at about 0.4% (US$979 million) of China’s agricultural imports of US$218 billion in 2023.

However, this current access in China is vital for the wool and red meat industry. China accounts for roughly 70% of South Africa’s wool exports. The fruit industry must be the next to see broader access.

There is a progressive increase in red meat exports, even though animal diseases currently cause glitches. The focus should be on expanding this access by lowering import duties/tariffs and other non-tariff barriers to encourage more fruit, grain, and other product exports to China.

Still, it is essential to emphasise that the focus on China is not at the expense of existing agricultural export markets and relationships. Instead, China offers an opportunity to continue with export diversification.

China is among the world’s leading agricultural importers, accounting for 9% of global agricultural imports in 2024 (before 2024, China had been a leading importer for many years). The US was the world’s leading agricultural importer in the same year, accounting for 10% of global imports.

Germany accounted for 7%, followed by the UK (4%), the Netherlands (4%), France (4%), Italy (3%), Japan (3%), Belgium (3%) and Canada (2%).

The diversity of agricultural demand in global markets convinces us that South Africa’s agricultural trade interests should not be limited to one country but should be spread across all major agricultural importers.

Importantly, promoting diversity and maintaining access to various regions have been key components of South Africa’s agricultural trade policy since the dawn of democracy.

For example, in 2024, South Africa exported a record US$13.7 billion of agricultural products, up 3% from the previous year. These exports were spread across the diverse regions. The African continent accounted for the lion’s share of South Africa’s agricultural exports, with a 44% share of the total value.

As a collective, Asia and the Middle East were the second-largest agricultural markets, accounting for 21% of the share of overall farm exports. The EU was South Africa’s third-largest agricultural market, accounting for a 19% share of the market. The Americas region accounted for 6% of South Africa’s agricultural exports in 2024. The rest of the world, including the United Kingdom, accounted for 10% of the exports.

So, while the recent protocol is commendable, wider access at lower tariffs is necessary. This export push is key to South Africa’s agricultural growth.

If you enjoyed this post, please consider subscribing to my newsletter here for free. You can also follow me on X (@WandileSihlobo)

He is a Senior Lecturer Extraordinary at the Department of Agricultural Economics at Stellenbosch University.

Sihlobo is also a Visiting Research Fellow at the Wits School of Governance, University of the Witwatersrand, and a Research Associate at the Institute of Social and Economic Research (ISER) at Rhodes University.

Sihlobo was appointed as a member of President Cyril Ramaphosa’s Presidential Economic Advisory Council in 2019 (and re-appointed in 2022), having served on the Presidential Expert Advisory Panel on Land Reform and Agriculture from 2018.

He is also a member of the Council of Statistics of South Africa (Stats SA) and a Commissioner at the International Trade Administration Commission of South Africa (ITAC).

Sihlobo is a columnist for Business Day, The Herald and Farmers Weekly magazine.

He holds a Bachelor of Science degree in Agricultural Economics from the University of Fort Hare and a Master of Science degree in Agricultural Economics from Stellenbosch University.