I have an opportunity to address members of the South African Parliament, mainly the portfolio committee responsible for agriculture, tomorrow, September 2, 2025. When I received the invitation to reflect on the sector’s operating conditions and the impact of geopolitics, I thought it would be a good opportunity first to highlight the changing structure of South Africa’s agriculture.

However, as I prepared my notes over the weekend, I realised that there are some vital policy matters to address in my speech, and I can perhaps present the key points about the sector’s structure succinctly in this letter.

The reason I am considering the structure of the sector is that I have seen, in several cases, pronouncements about South Africa’s agriculture that don’t accurately reflect its reality. Such instances remind me of the concept of “Zombie ideas“, which was popularised by the Nobel laureate, the economist, Paul Krugman, which is also the title of his new book, Arguing with Zombies.

This term refers to “ideas that keep being killed by evidence but shamble relentlessly forward, essentially because they suit a political agenda”.

We have many such “zombie ideas” in South Africa’s agriculture. This may seem petty, but some of the things I have heard, for example, are that:

South Africa has more or less 40,000 commercial farmers

Then there are more or less 2.5 million small-scale farmers

And a further 2.75 million people who perform some form of agricultural activity for home consumption or sale to the market

This is all incorrect.

My joint work with Professor Johann Kirsten of the Bureau for Economic Research (BER) has, over the years, endeavoured to reduce inaccuracies about land reform and the size and structure of the agricultural sector. Some of these efforts are evident in our chapter in the Oxford University Handbook on the South African Economy, in our latest book, The Uncomfortable Truth about South Africa’s Agriculture, and in numerous newspaper columns.

First, we need to deal with definitions:

A commercial farmer is any individual, entity, or household involved in agricultural production with the intention of selling to the market and therefore buys inputs to produce the commodity.

Large farmer: typically a farming enterprise that has an annual commercial turnover of R22,5 million or more.

Medium-scale farmer: Commercial turnover of between R13,5 million and R22,5 million

Small and micro farms (commercial): Turnover below R13.5 million.

Subsistence farmer/household: A Household that produces mainly for home consumption, usually in addition to social grants and migrant wages. Virtually no commercial sales.

Household: There should be roughly 4 to 6 people per household.

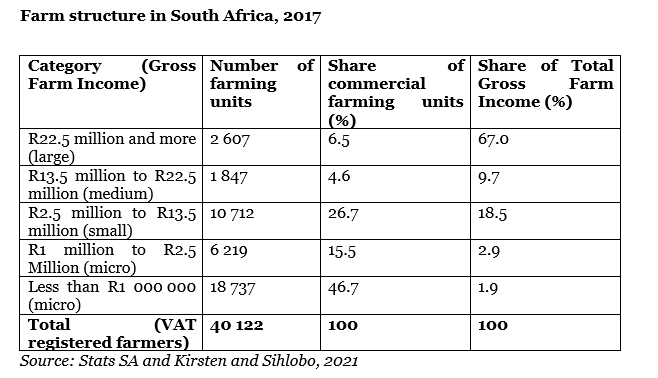

Here is the thing. The 2017 Census of Commercial Agriculture used the 40,102 farming enterprises registered for VAT as the sample frame. As we will show later, not all commercial farmers are registered for VAT, as the current threshold for VAT registration with the South African Revenue Service (SARS) is R1 million in annual turnover.

Fact: The 40,000 figure only refers to VAT-registered farm enterprises. They are distributed according to the definitions as shown in the Table below. Approximately 46% of all commercial farms (the majority of which are owned by white individuals) registered for VAT are classified by Statistics South Africa (Stats SA) as micro-enterprises or family farms.

We are fortunate that Stats SA released the latest numbers on agricultural households on 31 July 2025, extracted from the 2022 Population Census. This makes for fascinating reading but also requires careful interpretation to avoid the same mistakes alluded to earlier.

The most crucial observation in the report can be summarised as follows:

Households producing only for sale (thus commercial farmers): 106,753

Households producing mainly for sale (also commercial): 177,530

Households primarily producing for own consumption and households only for own consumption: 2,2 million (this is subsistence farmers, backyard gardeners and livestock keepers with few chickens and other animals)

In summary, these data indicate that South Africa has 284,283 commercial farming households, as estimated from the agricultural questions in the 2022 population census. This number corresponds to the 254,956 farming households we reported in our chapter in the Oxford University Handbook on the South African Economy, which we estimated from the 2017 Agricultural Census and the 2016 community survey.

So, we can now kill the “Zombie ideas” in South Africa’s agriculture by remembering the following facts:

Fact 1: There are 284,283 commercial farming households in South Africa, of which only 40,000 are registered for VAT.

Fact 2: 98.5% of these households are classified as small and micro farm enterprises

Therefore, as we engage with agricultural matters, we must be cognizant that it is a sizable sector, with many farmers who are commercialised. Importantly, the sector serves a large number of people. Therefore, policy-making in the sector must be rooted in reality, and we must avoid leaning on “zombie ideas”.

If you enjoyed this post, please consider subscribing to my newsletter here for free. You can also follow me on X (@WandileSihlobo)

It is easy to take for granted the gains we have achieved in South Africa’s agriculture, and for some, not to recognise that the very interventions from many organisations, especially those related to agrochemical use and advancement in breeding, have helped deliver this progress.

Some of the aspects one often sees are calls for restrictions on certain agrochemicals or slow progress in registering new agrochemicals by regulators.

The safety of agrochemical use is vital, and the optimal use while taking care of the environment is also key. This is what the discussion should be about, urging farmers to continue with safety practices and to avoid excessive use of any input.

However, the outright calls for restrictions on some inputs are typically misguided, and some compare our practices with those in Europe or other regions without appreciating that any input use is partly dependent on the environment in which we operate and the diseases or deficiencies we face.

On matters of products, we can’t always apply what happens in different geographies here. The key obsession for us in South Africa should be an embrace of science to improve our agricultural output and productivity, while ensuring safety and optimal use of inputs.

The regulators must also share the same objective: to embrace science and ensure that South Africa remains at the forefront of agricultural progress.

We are a semi-arid country, and we are witnessing an increasing number of disease outbreaks in crops and animals. One way of adapting will be through an embrace of science. We cannot hesitate on such important aspects for our food security and the progress of our rural economy.

If you enjoyed this post, please consider subscribing to my newsletter here for free. You can also follow me on X (@WandileSihlobo)

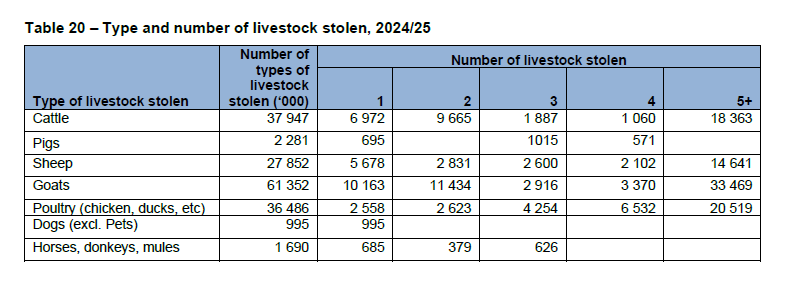

The one issue I haven’t written about, but is increasingly a challenge in some areas, is stock theft and crop and fruit theft. The data on some of these issues is scant, but I was reminded of this this morning when Statistics South Africa released its Governance, Public Safety, and Justice Survey results. In the agricultural section, Statistics South Africa indicated that in 2024/25, there were over 61,000 goats stolen, followed by cattle (37,947), then poultry (36,486).

Statistics South Africa also provided a valuable table below, which illustrates the locations where theft of livestock occurred and the type of livestock that was stolen in 2024/25.

We can see here that nearly half of the incidences occurred in a kraal/outside the house, followed by when livestock is in the fields/grazing land (40,7%).

In terms of what the thieves are after, we can see that the goats (39,8%) were the most common livestock that was stolen, followed by cattle (24,6%) in 2024/25.

If we want to continue having a prosperous agricultural sector, we must put strong control on these issues. This could be through enhanced collaboration between the police services and organised agriculture groups.

The theft indecencies present enormous costs to farmers and agribusinesses. In fact, if one talks to any commercial farmer, they would learn that over time, there is significant spending on security. I have seen several farmers installing cameras and several security measures due to concerns about crime.

For new entrant farmers, who may also have a relatively weak financial muscle, stock theft may take some out of business. The same is true for smallholder farmers who are also victims of such crimes, leaving households in a worse-off position.

We must also not forget that South Africa continues to view agriculture as one of the key sectors to our long-term growth agenda. To achieve the long-term growth objectives, we not only need the release of over two million hectares of government land to farmers with title deeds, but also an increase in investment. The investment will increase if there is comfort about the security in our sector. Thus, issues of crime must also be prioritised and addressed swiftly.

We are also at a space where we, as a country, are encouraging young people to join the sector. For the young and new entrant farmers to thrive and have confidence in the sector, there must be a security improvement. Therefore, fighting crime should remain a top priority in collaboration with organised agriculture.

Agriculture is an essential sector of our economy, with great potential for job creation and improvement of economic conditions in rural South Africa; therefore, ensuring that farmers are operating in a safe and sound environment is key.

If you enjoyed this post, please consider subscribing to my newsletter here for free. You can also follow me on X (@WandileSihlobo)

As someone who spends a bit of time thinking about agricultural development and efficiency gains among existing commercial farmers, it is always encouraging to encounter new organisations that are focused on this goal.

Earlier today, I made a brief stop at Khula!, an agri-tech company based in Johannesburg. This was not my first engagement with Khula; I had engaged with the team deeply in the early stages of their work.

But after some years, it was refreshing to listen to their team talk about the various offerings to support farmers and the improvements they make in the efficiencies in the different value chains of our sector. Khula’s work on farm inputs provision, commodities and fresh produce trading, and off-taking of the produce, amongst other things, is all essential to the agricultural industry.

Importantly, they are not only assisting small-scale or exclusively large-scale farmers; their product offering is valuable for all types of farmers. They also cover most commodities, and do not only focus on one subsector.

This is not a sponsored post; I don’t do those. But I felt it was important that I highlight Khula in case some people who read these letters are not aware of young entities like Khula, which are already making great strides.

Khula’s leadership is young and vibrant, and it was very inspiring to listen to them and hear their vision and enthusiasm about South Africa’s agriculture and the entire food, fibre, and beverages value chains.

Of course, the agri-tech companies cannot stand on their own; they are the service providers, which means their growth depends on the support of the various stakeholders. Equally, the various sector stakeholders could realise some efficiency gains when bringing in or collaborating with various agri-tech organisations.

The success of the South African agricultural sector is reliant on the efforts of many organisations and individuals, including scientists, breeders, seed companies, machinery suppliers, financiers, input suppliers, agribusinesses, traders, and many more valuable organisations and service providers.

The agri-tech new firms add to this line of organisations that sustain this critical sector of our economy that we all take pride in, which has more than doubled since 1994 in value, with exports at nearly US$14 billion a year, and made South Africa the only African country in the top-40 global agricultural exporters.

I have mentioned Khula here, but we have many other young agri-tech companies in South Africa, such as OneFarm Share, AgrigateOne, Nile, and Agrimall, among others. I know I have skipped a few (apologies).

If you enjoyed this post, please consider subscribing to my newsletter here for free. You can also follow me on X (@WandileSihlobo)

In about three weeks, on September 9, Statistics South Africa will release the GDP data for the second quarter of 2025. One of the sectors that some are likely observing closely, because of its significant influence on our fortunes in recent years, is agriculture.

In the first quarter of the year, the sector’s performance was pleasing; the agricultural gross value added expanded by 15,8% quarter-on-quarter (seasonally adjusted). This expansion was primarily due to the improved performance of certain field crops and the horticulture subsectors.

But as the close observers of the sector know, the quarterly data tend to be somewhat volatile, influenced by times of harvest and crop deliveries, amongst other factors. It is particularly such issues that I remain slightly concerned that the second quarter performance may not be as robust as the start of the year.

We had a delay in our summer grain harvest, with more momentum happening at the start of the third quarter than usually in the second quarter of the year. Indeed, we have ample summer grain and oilseeds, estimated at 18.74 million tonnes (up 21% year-on-year). But the season was late by roughly a month and a half because of the excessively prolonged summer rains, amongst other factors.

We have also continued to struggle with the foot and mouth disease and a few avian influenza cases, particularly in the second quarter. It was at the end of the second quarter that the foot and mouth disease vaccines arrived in South Africa for the start of the vaccination campaign.

It is particularly these factors that we must reflect on, seriously, as we formulate or assess the narrative behind the agricultural performance in the second quarter of 2025’s data, which will be released on September 9.

But of course, not all crops were late. The citrus harvest season started in the second quarter, and we have an ample harvest. Farmers moved quickly to take advantage of the tariff pause window in the U.S., which allows for faster harvesting and adds to the upside in our thinking about the second quarter performance.

With all these factors considered, the critical point is that we remain convinced that 2025 will likely be a recovery period for South Africa’s agriculture. But, as we have communicated on various occasions, it will be an uneven recovery.

The livestock industry continues to struggle with foot and mouth disease, and a few cases of avian influenza in poultry. Meanwhile, on the upside, the field crops, mainly grains, oilseeds and sugarcane, all expect a fantastic recovery from last season. We also have an excellent harvest of fruits and vegetables.

But in terms of quarterly growth, the agricultural sector may show a slight slowdown in the second quarter, following a 15,8% quarter-on-quarter (seasonally adjusted) in the first quarter of 2025. I am not talking about contraction, but modest growth. This is because of the late harvest and grain deliveries to silos.

Still, this won’t change our view that on an annual basis, 2025 is a recovery period for South Africa’s agriculture.

If you enjoyed this post, please consider subscribing to my newsletter here for free. You can also follow me on X (@WandileSihlobo)

He is a Senior Lecturer Extraordinary at the Department of Agricultural Economics at Stellenbosch University.

Sihlobo is also a Visiting Research Fellow at the Wits School of Governance, University of the Witwatersrand, and a Research Associate at the Institute of Social and Economic Research (ISER) at Rhodes University.

Sihlobo was appointed as a member of President Cyril Ramaphosa’s Presidential Economic Advisory Council in 2019 (and re-appointed in 2022), having served on the Presidential Expert Advisory Panel on Land Reform and Agriculture from 2018.

He is also a member of the Council of Statistics of South Africa (Stats SA) and a Commissioner at the International Trade Administration Commission of South Africa (ITAC).

Sihlobo is a columnist for Business Day, The Herald and Farmers Weekly magazine.

He holds a Bachelor of Science degree in Agricultural Economics from the University of Fort Hare and a Master of Science degree in Agricultural Economics from Stellenbosch University.