It is very early to tell what the 2025-26 summer crop season may look like. The farmers will start tilling the land next month, mainly for summer grains and oilseeds.

Remember, we produce all of South Africa’s vegetables and fruits under irrigation. Therefore, when we talk of the rainy season, we typically have in mind grains, oilseeds, and other field crops, such as sugarcane. We also think of grazing veld for livestock. And yes, the rainy season matters for dam levels.

Therefore, when the 2025-26 summer crop season begins next month, in October, we will also intensify our focus on the weather outlook, as it may be a crucial factor to consider when assessing the production outlook.

It is in this regard that I was encouraged to read the South African Weather Service’s (SAWS) Seasonal Climate Watch report, released on 1 September 2025. The SAWS stated that:

“The El Niño-Southern Oscillation (ENSO) is firmly in a neutral state; however, predictions indicate that we may be moving towards a weak La Niña event during the coming summer season.”

Such an optimistic outlook would signal prospects of above normal rainfall, which is favourable for agriculture.

Admittedly, the SAWS were quick to add that:

“It is still a bit too early to make any reliable conclusions on ENSO’s effect during early summer; more reliable interpretations can only be made in the next couple of months as the prediction systems become more reliable.”

This is a fair point. But equally comforting. Remember, we are emerging from a La Niña, which helped ensure a robust maize harvest of 15.80 million tonnes, a 23% increase year-on-year, primarily due to expected annual yield improvements.

During this period, we often fear that the La Niña season may be followed by its opposite, an El Niño, which typically brings below-normal rainfall.

Therefore, as long as there is no mention of a strong El Niño possibility, we look forward to the 2025-26 summer season with optimism for South Africa’s agriculture.

If you enjoyed this post, please consider subscribing to my newsletter here for free. You can also follow me on X (@WandileSihlobo)

I have an opportunity to address members of the South African Parliament, mainly the portfolio committee responsible for agriculture, tomorrow, September 2, 2025. When I received the invitation to reflect on the sector’s operating conditions and the impact of geopolitics, I thought it would be a good opportunity first to highlight the changing structure of South Africa’s agriculture.

However, as I prepared my notes over the weekend, I realised that there are some vital policy matters to address in my speech, and I can perhaps present the key points about the sector’s structure succinctly in this letter.

The reason I am considering the structure of the sector is that I have seen, in several cases, pronouncements about South Africa’s agriculture that don’t accurately reflect its reality. Such instances remind me of the concept of “Zombie ideas“, which was popularised by the Nobel laureate, the economist, Paul Krugman, which is also the title of his new book, Arguing with Zombies.

This term refers to “ideas that keep being killed by evidence but shamble relentlessly forward, essentially because they suit a political agenda”.

We have many such “zombie ideas” in South Africa’s agriculture. This may seem petty, but some of the things I have heard, for example, are that:

South Africa has more or less 40,000 commercial farmers

Then there are more or less 2.5 million small-scale farmers

And a further 2.75 million people who perform some form of agricultural activity for home consumption or sale to the market

This is all incorrect.

My joint work with Professor Johann Kirsten of the Bureau for Economic Research (BER) has, over the years, endeavoured to reduce inaccuracies about land reform and the size and structure of the agricultural sector. Some of these efforts are evident in our chapter in the Oxford University Handbook on the South African Economy, in our latest book, The Uncomfortable Truth about South Africa’s Agriculture, and in numerous newspaper columns.

First, we need to deal with definitions:

A commercial farmer is any individual, entity, or household involved in agricultural production with the intention of selling to the market and therefore buys inputs to produce the commodity.

Large farmer: typically a farming enterprise that has an annual commercial turnover of R22,5 million or more.

Medium-scale farmer: Commercial turnover of between R13,5 million and R22,5 million

Small and micro farms (commercial): Turnover below R13.5 million.

Subsistence farmer/household: A Household that produces mainly for home consumption, usually in addition to social grants and migrant wages. Virtually no commercial sales.

Household: There should be roughly 4 to 6 people per household.

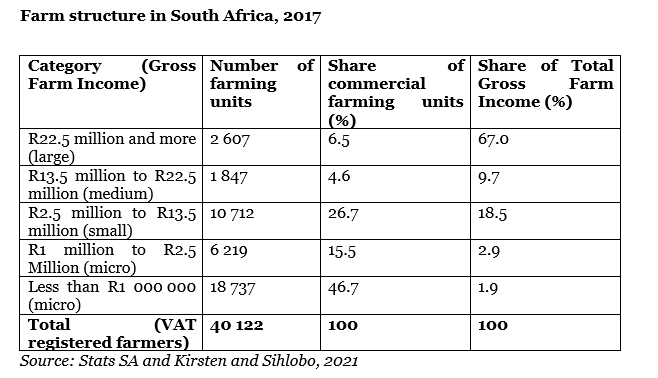

Here is the thing. The 2017 Census of Commercial Agriculture used the 40,102 farming enterprises registered for VAT as the sample frame. As we will show later, not all commercial farmers are registered for VAT, as the current threshold for VAT registration with the South African Revenue Service (SARS) is R1 million in annual turnover.

Fact: The 40,000 figure only refers to VAT-registered farm enterprises. They are distributed according to the definitions as shown in the Table below. Approximately 46% of all commercial farms (the majority of which are owned by white individuals) registered for VAT are classified by Statistics South Africa (Stats SA) as micro-enterprises or family farms.

We are fortunate that Stats SA released the latest numbers on agricultural households on 31 July 2025, extracted from the 2022 Population Census. This makes for fascinating reading but also requires careful interpretation to avoid the same mistakes alluded to earlier.

The most crucial observation in the report can be summarised as follows:

Households producing only for sale (thus commercial farmers): 106,753

Households producing mainly for sale (also commercial): 177,530

Households primarily producing for own consumption and households only for own consumption: 2,2 million (this is subsistence farmers, backyard gardeners and livestock keepers with few chickens and other animals)

In summary, these data indicate that South Africa has 284,283 commercial farming households, as estimated from the agricultural questions in the 2022 population census. This number corresponds to the 254,956 farming households we reported in our chapter in the Oxford University Handbook on the South African Economy, which we estimated from the 2017 Agricultural Census and the 2016 community survey.

So, we can now kill the “Zombie ideas” in South Africa’s agriculture by remembering the following facts:

Fact 1: There are 284,283 commercial farming households in South Africa, of which only 40,000 are registered for VAT.

Fact 2: 98.5% of these households are classified as small and micro farm enterprises

Therefore, as we engage with agricultural matters, we must be cognizant that it is a sizable sector, with many farmers who are commercialised. Importantly, the sector serves a large number of people. Therefore, policy-making in the sector must be rooted in reality, and we must avoid leaning on “zombie ideas”.

If you enjoyed this post, please consider subscribing to my newsletter here for free. You can also follow me on X (@WandileSihlobo)

Some countries in the Southern Africa region have some maize supplies from the recent harvest. South Africa is likely to see its exports slow down for now, particularly to countries in the region. We may continue to see encouraging export volumes to the Far East and other areas of the world.

Still, towards the end of the year and into 2026, when domestic supplies are somewhat depleted in the various countries in the region, they will return to the market and import maize. This was not the case last season, as most countries were negatively affected by the drought and required massive imports throughout. This time around, we had favourable summer rains that supported grain production across the Southern Africa region.

It is this brief context that we must keep in mind when observing maize export data these days. The exports aren’t down because our maize is expensive; in fact, maize prices have been under pressure in recent weeks as farmers delivered decent maize volumes to silos, and South Africa expects an ample harvest of 15.80 million tonnes, which is 23% higher than the crop for the 2023-24 season.

It is against this background that, for example, maize exports for the past week were mediocre. For example, South Africa exported 14,428 tonnes of maize in the week of August 22, all of which was destined for the Southern African region.

This placed South Africa’s 2025-26 maize exports at 553,808 tonnes, out of the expected seasonal exports of 2.12 million tonnes. The current marketing year only ends in April 2026.

If you enjoyed this post, please consider subscribing to my newsletter here for free. You can also follow me on X (@WandileSihlobo)

The US’s decision to impose a steep tariff on imports from SA has ignited an urgent discussion on how best to minimise the effect of these measures on various exporting sectors, including agriculture.

In addition to the ongoing conversation about expanding SA’s agricultural export markets, we believe the country must accelerate its efforts to promote agricultural products in international markets.

The Department of Trade, Industry and Competition typically leads the various trade shows, supported by the private sector and other government agencies. These trade shows, more than ever, must be channelled to the priority regions for our export expansion plan.

The visibility of the high-quality variety of SA agricultural products is key for marketing purposes and informing consumers and retailers in various countries about the products they could source from SA. We believe such marketing work and formal trade conversations would be a powerful approach for ensuring the penetration of the SA agricultural products into a range of new markets.

Importantly, government officials in SA, particularly those in the Department of Agriculture responsible for export-related matters, should also share a sense of urgency for promoting exports. They should work collaboratively to assist exporting businesses rather than creating more bureaucratic hindrances, while the global interest is established.

We have heard of a few cases where there is often a lack of collaboration from the domestic side, while international consumers are open to SA products, particularly for some processed products. A case in point is the pet food industry, where local authorities often move much more slowly than exporters would like.

While SA is thriving in Africa and Europe, which account for roughly two-thirds of its agricultural exports in value terms, there remains room for expansion in other regions. Asia the Middle East are some of the areas we continue to see greater opportunity for export expansion. During various government visits to these regions, bringing the private sector along for deeper business engagement and optimising existing structures for trade shows should be explored.

Also critical in this trade conversation is the appropriate staffing of embassies in the key export markets. The support staff at the embassies must have the proper skillset to assist the SA businesses in their commercial activities. Indeed, the guidelines of the work must be outlined in SA’s economic diplomacy strategy, spelling out both the country’s economic and commercial diplomacy focus. Such a vision and strategy would then guide the work of the support staff.

The discussions on trade policy cannot be limited to the Department of Trade, Industry and Competition alone. They require a comprehensive approach to ensure the agreements are rooted in the aspirations of business and national priorities. Importantly, these engagements create a platform for executing trade and increasing the visibility of SA agricultural products in the world market.

This sector of the economy still has potential to create more jobs at the primary level and in the value chains. However, the employment and sustainability of the industry depend on a comprehensive growth approach. Maximising trade opportunities is key to ensuring that we continue on an export-led growth approach.

There is also a need to ensure that the exporting industries are well supported. As such, a deeper involvement of officials in SA’s various embassies is even more critical as the country strengthens its export approach, particularly for agricultural and other exporting sectors of the economy.

This new path requires a well-communicated and supported economic diplomacy strategy for the country, along with the alignment of all necessary interventions to support it. All these priorities are in recognition of the role of agriculture in supporting SA’s economic growth.

If you enjoyed this post, please consider subscribing to my newsletter here for free. You can also follow me on X (@WandileSihlobo)

Yesterday, August 27, we participated in the NATIONAL FARM WORKERS’ PLATFORM 2025 in Cape Town (virtually). We provided input on the State of the South African farming economy, with an emphasis on trade matters and job prospects.

In terms of employment, the sector remains a major employer, with 906,000 working in primary agriculture (well above the long-term average of 799k jobs), and over 200,000 in the value chain. The current trade friction, particularly in the US, is a concern, but we remain optimistic that the sector will show growth this year and maintain generally healthy employment levels.

In agricultural conditions, the field crops, mainly grains, oilseeds and sugarcane, all expect a fantastic recovery from last season’s drought. We also have an excellent harvest of fruits and vegetables. All these are supportive of work opportunities in the sector.

On the downside, the livestock industry continues to struggle with foot-and-mouth disease, as well as a few cases of avian influenza in poultry.

Still, the better field crop and horticulture production conditions should continue to support employment. At the same time, the negotiations for South Africa to secure better tariff levels in the US continue.

Some of the matters the farmworkers raised were around (1) the fears for their jobs, given the talks of trade friction (they realise the importance of trade to sustain the farming businesses), (2) agrochemicals and the need for more information about their safe applications, etc. This is something farmers and stakeholders are focusing on—the safe and optimal use of agrochemicals, which are key for our farm productivity. (3) There were also questions about the general technological innovation in the sector. (4) Some raised concerns about the “seasonal hunger/poverty” issues in rural South Africa.

Overall, it was an encouraging conversation and exchange after our formal speech. We emphasised that the sector still has a great deal to offer, and the roughly one million jobs highlighted in the National Development Plan as a possibility in agriculture could still materialise. The prerequisites include the release of approximately 2.5 million hectares of government land to appropriately selected beneficiaries with title deeds, as well as improvements in land governance in the former homelands, among other interventions. At the core, collaboration between government, organised labour, and business is key.

If you enjoyed this post, please consider subscribing to my newsletter here for free. You can also follow me on X (@WandileSihlobo)

Minimal government intervention in agricultural markets is often considered an ideal policy path, as government intervention may disrupt the efficient allocation of scarce resources or functioning of the market (through the forces of supply and demand).

In times of abundant harvests, farmers and agribusinesses must be allowed to export and benefit from the global market. In times of droughts or floods, trade must still be allowed. Indeed, there may be short-term economic pain for consumers through higher prices in deficit years when imports are needed, but this induces farmers to plant more in the coming seasons.

At times, governments ban imports to protect local farmers when they have ample domestic supplies, which are deemed sufficient to meet consumer requirements. However, that also limits the consumer’s choice and artificially increases the domestic price by restricting more competitively priced imports.

I am highlighting these policy tradeoffs in light of recent news from Zimbabwe. A report by Reuters, a news organisation, suggests that the Zimbabwean government has reinstated a ban on maize imports. The government believes that in the interim, there are sufficient supplies for the local market and wants to ensure maximum price realisation for the domestic producers before allowing imports.

Nevertheless, it remains unclear if Zimbabwe has sufficient maize supplies for the year or will need imports later. Zimbabwe’s 2024-25 maize production is forecast at 1.3 million tonnes, according to recent data from the Pretoria-based unit of the United States Department of Agriculture (USDA). This is just more than twice the output from the previous season, which was a drought period.

This recovery in Zimbabwe’s maize production is primarily driven by improved weather conditions and an increase in the area that farmers managed to plant for maize. If this production level materialises, then the ban may be temporary.

Zimbabwe’s potential maize harvest of 1.3 million tonnes will not be sufficient to meet the country’s domestic needs of 2.0 million tonnes per annum, leaving it to import the balance.

In the last marketing year, South Africa supplied nearly all of Zimbabwe’s maize imports. However, in the 2025-26 marketing year, there may be some changes, with Zambia regaining its net exporter status as it expects a bumper harvest of 3.66 million tonnes. This far surpasses Zambia’s maize consumption of 2.8 million tonnes per annum.

South Africa also forecasts a robust maize harvest of 15.80 million tonnes, which is 23% higher than the previous 2023-24 season’s crop. These forecasts are well above South Africa’s annual maize needs of approximately 12.00 million tonnes, implying that South Africa will have a surplus and remain a net exporter of maize.

For South African maize exporters, the message here is that Zimbabwe may not be the ideal market in the near term, as they have ample domestic supplies. However, later in the season, they may return to the market and import. The USDA forecasts suggest that the expected crop is insufficient to last throughout the year.

If you enjoyed this post, please consider subscribing to my newsletter here for free. You can also follow me on X (@WandileSihlobo)

He is a Senior Lecturer Extraordinary at the Department of Agricultural Economics at Stellenbosch University.

Sihlobo is also a Visiting Research Fellow at the Wits School of Governance, University of the Witwatersrand, and a Research Associate at the Institute of Social and Economic Research (ISER) at Rhodes University.

Sihlobo was appointed as a member of President Cyril Ramaphosa’s Presidential Economic Advisory Council in 2019 (and re-appointed in 2022), having served on the Presidential Expert Advisory Panel on Land Reform and Agriculture from 2018.

He is also a member of the Council of Statistics of South Africa (Stats SA) and a Commissioner at the International Trade Administration Commission of South Africa (ITAC).

Sihlobo is a columnist for Business Day, The Herald and Farmers Weekly magazine.

He holds a Bachelor of Science degree in Agricultural Economics from the University of Fort Hare and a Master of Science degree in Agricultural Economics from Stellenbosch University.