In two months, farmers across South Africa will begin tilling the land for the 2025-26 summer grain and oilseed season. However, for now, we still have our eyes on the 2024-25 season, which is nearing its end.

This afternoon, on August 27, South Africa’s Crop Estimates Committee increased the country’s 2024-25 summer grains and oilseeds production estimate by 4% from last month, to 19.55 million tonnes.

This estimate comprises maize, sunflower seeds, soybeans, groundnuts (peanuts), sorghum, and dry beans. There is an annual uptick in all the crops, mainly supported by favourable summer rains and the decent area plantings. The base effects also help, as we struggled with a drought last year that weighed on the harvest.

This ample crop will likely continue to put downward pressure on prices, which bodes well for a moderating path of consumer food price inflation.

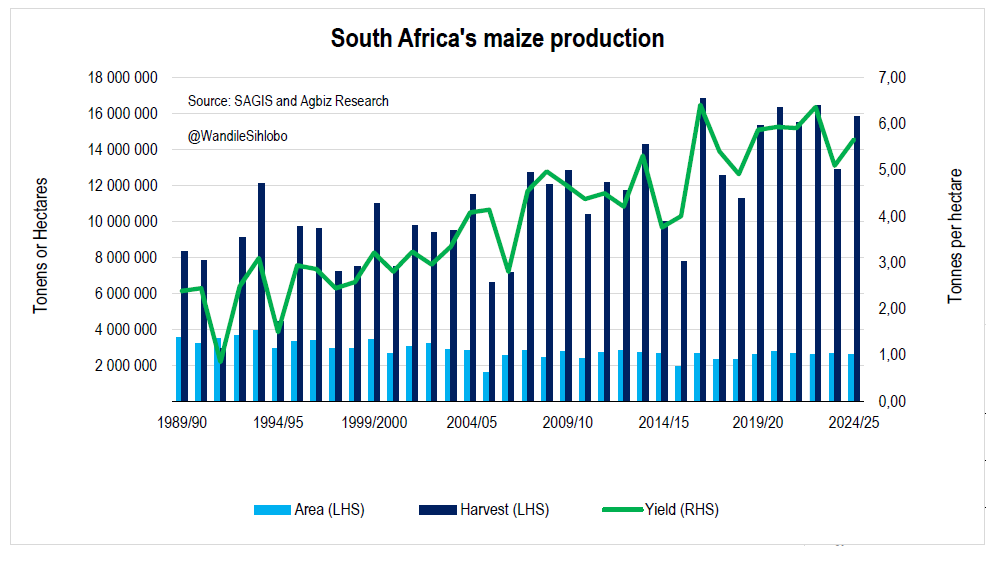

If I were to highlight one crop to underscore my point about food inflation, it would be maize. South Africa’s 2024-25 maize harvest is now forecast at 15.80 million tonnes, which is 23% higher than the 2023-24 season’s crop.

Importantly, these forecasts are well above South Africa’s annual maize needs of approximately 12.00 million tonnes, implying that South Africa will have a surplus and remain a net exporter of maize.

In essence, we are in another year of abundance in grain production, despite the quality issues in the white maize and sunflower seed regions.

If you enjoyed this post, please consider subscribing to my newsletter here for free. You can also follow me on X (@WandileSihlobo)