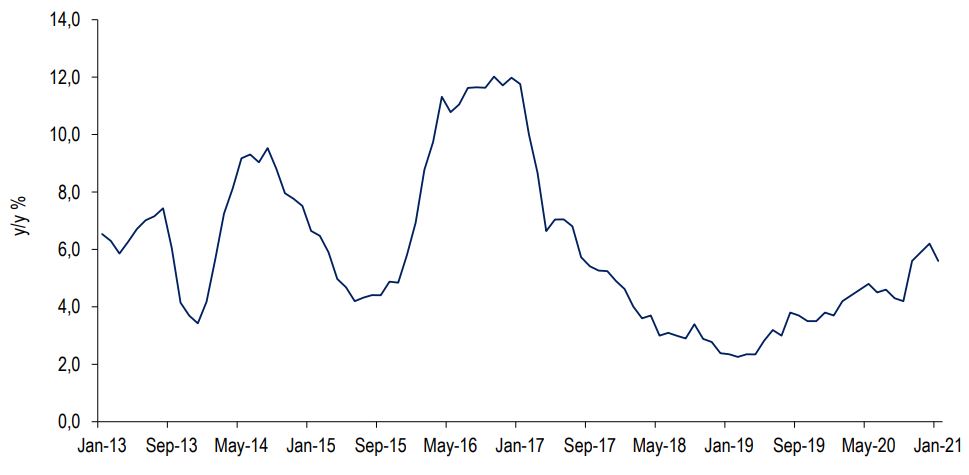

South Africa’s food price inflation softened to 5,6% y/y in January 2021, from 6,2% y/y in the previous month. The deceleration was in most product prices in the food basket except for bread and cereals, which accelerated from the levels seen in December 2020. Nevertheless, this was overshadowed by the slowing price inflation in meat; fish; milk, eggs and cheese; fruit; and vegetables.

The “bread and cereals” products price inflation mirrors the increases observed in the past few months in grain prices. The current slightly elevated price inflation for this particular product prices will likely prevail for most of the first quarter as grain prices have continued to surge since the start of the year. While South Africa had its second-largest grains harvest in history in the 2019/20 production season, and ordinarily one would have expected prices to soften, we have experienced the opposite. Grain prices remained elevated on the back of strong demand for South African maize across the Southern Africa region and the Far East markets. The weaker domestic currency also added to the price increase and spillovers from higher global grains prices. The global grains market was primarily driven by the growing demand for grains in China.

Nevertheless, we expect South Africa’s grain prices to soften from the second quarter on the back of an expected sizeable domestic maize harvest of 16,6 million tonnes from 15,4 million tonnes in 2019/20 production season. This is all against South Africa’s annual consumption of about 11,4 million tonnes.

Meat, which has a higher weighting of 35% in the food basket, saw price inflation decelerating in January 2021, in part, due to increased supply following slightly higher slaughtering activity in December 2020. Cattle slaughtering was up by 1% in December 2020, at 281 043 head. This slight increase, combined with relatively depressed household incomes, has partly contributed to softening price inflation for the product. In terms of vegetables and fruit, the domestic supply recovery is mainly the contributing factor to easing price inflation.

From now on, we still expect South Africa’s food price inflation to remain at slightly elevated levels in the first quarter of the year because of higher grain prices and the imported vegetable oils and fats. But from the second quarter of the year, grain prices could soften and filter through, with a lag, on the “bread and cereals” products prices. This product category also has a higher weighting of 21% in the food basket, and changes in its price inflation will be noticeable. In terms of meat, we expect a sideways price movement for the coming months. Slaughtering could slightly improve in 2021 in cattle, and the base effects on poultry meats, which increased in 2020 partly as a result of an import tariff hike, could also bode well for food price inflation.

In sum, we believe South Africa’s food price inflation could remain relatively higher in the first quarter of 2021, primarily underpinned by bread and cereals products (the pass-through of current higher grains prices will persist for the first quarter). But from the second quarter, we could see food price inflation decelerating somewhat. Our baseline view is for food price inflation to average around 5,0% y/y in 2021.

Follow me on Twitter (@WandileSihlobo).